Click Here to Earn $5-200 In Free Stock!

The Impacts of Lower Interest Rates on the Economy

Daniel Williams

11/7/20246 min read

What are Interest Rates?

Interest rates represent the cost of borrowing money or the return on investment for savings and are typically expressed as a percentage. They play a crucial role in the economy, influencing various financial decisions made by individuals, businesses, and governments. Interest rates are predominantly determined through the interaction of supply and demand in the money market, alongside monetary policy decisions made by the central bank, such as the Federal Reserve in the United States.

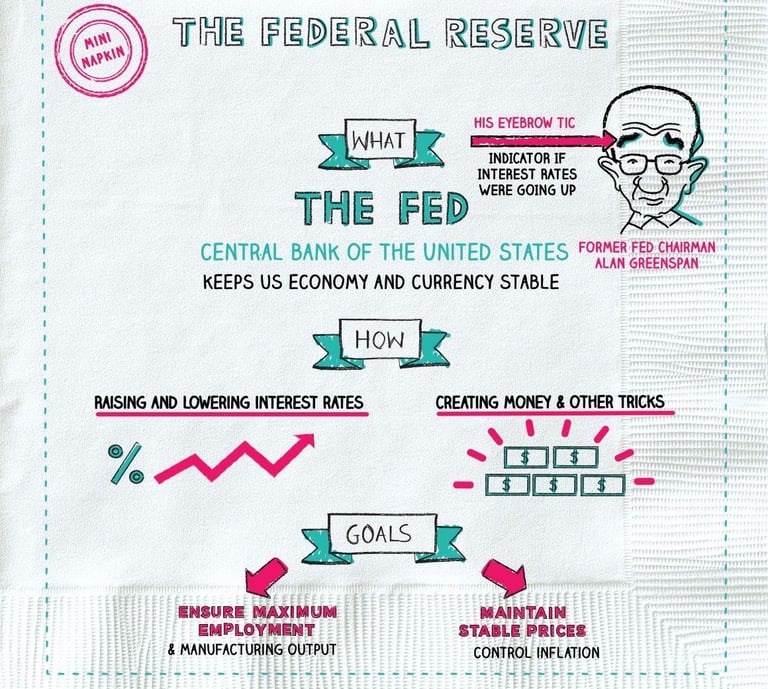

The Federal Reserve, often referred to as the Fed, possesses the authority to set key interest rates, particularly the federal funds rate, which is the rate at which banks lend to each other overnight. This rate acts as a benchmark for other rates, impacting everything from mortgage rates to credit card interest. When the Fed decides to either raise or lower the federal funds rate, it directly affects broader economic activity. For instance, lowering interest rates can stimulate economic growth by making borrowing cheaper, thereby encouraging spending and investment. Conversely, higher rates typically aim to curb spending and control inflation.

The recent cuts in interest rates are particularly noteworthy, especially as they followed closely after the election period. This timing can reflect a desire to boost economic confidence and support recovery during uncertain times. When analyzed in basis points—a unit of measure equating to one-hundredth of a percentage point—these adjustments in the federal funds rate can significantly alter lending behaviors and, ultimately, the economic landscape. A cut of 25 basis points, for example, may seem minor but can have substantial implications for the overall economy, enhancing liquidity and consumer spending. Thus, understanding the mechanics behind interest rates is vital for comprehending their impacts on economic activity.

The Federal Reserve's Recent Rate Cuts

The Federal Reserve's decision to cut interest rates is often a response to evolving economic conditions, and the recent adjustments have sparked considerable discussion among economists and market participants. In the months following the recent election, the Fed scrutinized various economic indicators, including employment rates, consumer spending, and inflation levels. These factors collectively informed the central bank's strategy to promote economic growth and stability through lower borrowing costs.

The anticipated cut of 25 basis points was primarily motivated by concerns surrounding sluggish economic growth and uncertainty in global markets. As inflation rates remained subdued, and wage growth showed signs of stagnation, the Federal Reserve sought to stimulate demand by making credit more accessible. Lower interest rates enable businesses to borrow more easily, leading to increased investment in expansion and productivity improvements. Similarly, consumers benefit from lower loan rates, which can encourage spending on big-ticket items such as homes and automobiles.

The implications of these rate cuts are multifaceted. For businesses, reduced interest rates can serve as an impetus for hiring and capital investments, fostering an environment conducive to economic growth. Conversely, consumers may experience an uptick in confidence, resulting in heightened consumer spending. This interplay between businesses and consumers is critical, as it ultimately drives economic activity and growth.

However, while lower interest rates carry numerous advantages, they can also present certain risks including asset bubbles and potential overheating of markets. The Federal Reserve must carefully monitor these developments as it navigates the delicate balance of stimulating the economy while ensuring long-term stability. The decision for further rate cuts will hinge on ongoing assessments of economic performance, and the Fed is poised to adapt its policies in response to any significant changes in the economic landscape.

Benefits of Lower Interest Rates for Everyday Consumers

Lower interest rates play a significant role in enhancing the financial well-being of everyday consumers, primarily through reduced borrowing costs. When interest rates decrease, the cost of borrowing diminishes, making it more accessible for individuals to take out loans for various purposes, including personal expenses, education, and investments. This ease of access to credit facilitates increased spending, which can contribute positively to the overall economy.

One of the most notable benefits for consumers is the lowering of mortgage rates. With reduced interest rates, homeowners can refinance existing mortgages or purchase new homes at more favorable terms. This can lead to substantial savings on monthly mortgage payments, allowing consumers to allocate funds toward other essential expenses, such as education, healthcare, or discretionary spending. Additionally, as mortgage costs decline, the housing market may experience increased activity, benefiting both buyers and sellers.

Furthermore, the reduction in interest rates improves consumer confidence, as individuals feel more secure in their financial situations. Lower interest obligations often result in consumers having more disposable income, which can stimulate spending in various sectors such as retail and services. This uptick in consumer spending can create a ripple effect throughout the economy, bolstering business revenues and potentially leading to job creation.

The impacts of lower interest rates extend beyond individual convenience, as they collectively foster a more dynamic economic environment. Sectors dependent on consumer borrowing, such as automotive and home improvement industries, may experience significant growth. In summary, the benefits of lower interest rates for everyday consumers are clear: reduced borrowing costs, lower mortgage rates, and enhanced consumer spending create an overall positive effect on both household finances and the economy as a whole.

Opportunities for Wealth Building

Lower interest rates present a unique opportunity for individuals aiming to build wealth. When central banks reduce interest rates, borrowing costs decrease, which can significantly alter financial strategies for both consumers and investors. One of the primary advantages of lower interest rates is the potential for refinancing existing loans, such as mortgages or student loans. By securing a lower rate, borrowers can reduce their monthly payments, thereby freeing up additional cash that can be redirected toward savings or investments. This not only improves cash flow but contributes to greater long-term wealth accumulation.

Moreover, individuals may find it advantageous to invest in assets that typically appreciate over time, such as real estate or stocks. With lower borrowing costs, purchasing property becomes more accessible, and the potential for appreciation can result in substantial financial returns. Investors may also be tempted to allocate capital towards the stock market, as lower interest rates can lead to increased consumer spending and economic activity, boosting corporate profits and, consequently, stock valuations.

In addition to these strategies, lower interest rates create an environment conducive to leveraging cheaper credit to fund new ventures or expand existing businesses. Entrepreneurs can take advantage of favorable borrowing conditions to invest in their operations, purchase equipment, or expand their workforce. This not only contributes to individual wealth-building efforts but also stimulates economic growth and job creation at the community level. Therefore, by understanding and utilizing the opportunities presented by lower interest rates, individuals can employ effective financial strategies to enhance their wealth over time.

Lower Rates Economic Impact

Lower interest rates play a pivotal role in fostering economic growth by making borrowing more attractive for businesses and consumers. When interest rates decrease, the cost of obtaining loans diminishes, providing both companies and individuals with increased access to credit. This enhanced liquidity often leads businesses to expand operations, invest in new technologies, and hire additional personnel, ultimately boosting overall productivity and encouraging a more vibrant economy.

As businesses become more confident in making capital investments, the ripple effect can be seen across various sectors. With lower borrowing costs, companies are more likely to embark on new projects, undertake research and development, or upgrade existing facilities. This not only contributes to individual business growth but also stimulates demand for raw materials and services, further invigorating the supply chain. Consequently, strong business investment spurs job creation, leading to an overall positive employment outlook, which is essential for sustained economic growth.

Furthermore, lower interest rates encourage consumer spending, as individuals are more willing to take out loans for significant purchases such as homes, cars, and appliances. With lesser financial constraints, consumers can make these investments, which in turn fosters demand for goods and services, enhancing revenue for businesses. The cycle of increased consumer spending stimulates production, thereby necessitating more hiring and further reinforcing economic growth.

In essence, the impact of lower interest rates on economic growth is multifaceted. By promoting business investments and consumer spending, lower interest rates catalyze job creation and enhance economic activity. When these factors combine, they contribute to a more robust economic environment, ultimately benefiting society as a whole through improved living standards and increased job opportunities.

What Lower Rates Could Mean for the Future

As lower interest rates persist, they are likely to shape the economic landscape for the foreseeable future. The Federal Reserve's current policy is geared towards stimulating growth, particularly following periods of low consumer spending and sluggish business investments. In this environment, one can expect ongoing discussions within the Fed regarding the balance of sustaining economic recovery while preventing inflation from spiraling. Economic indicators such as unemployment rates, consumer confidence indices, and inflation measurements will play pivotal roles in guiding these discussions.

One of the primary implications of sustained lower interest rates is their potential effect on consumer behavior. With borrowing becoming more affordable, individuals might be incentivized to take out loans for significant investments such as homes or cars, leading to an uptick in overall economic activity. However, potential consumers must also remain cautious about accumulating debt, as interest rates ultimately influence repayment burdens. For investors, the low-rate environment could signal a shift towards equities or other asset classes that historically outperform in expansive fiscal climates.

The landscape for savings accounts and fixed-income investments will also evolve. Many investors may find the lower returns on government bonds and savings accounts unappealing, pushing them to explore alternative investing avenues. This shift could lead to increased volatility in the stock market, as more capital floods into equities. Furthermore, industries heavily reliant on borrowing—such as real estate and construction—are likely to benefit from these low rates, which can stimulate job creation and development projects.

In conclusion, the lower interest rate environment presents diverse opportunities and challenges for both consumers and investors. By staying informed about economic conditions and adjusting strategies accordingly, stakeholders can position themselves advantageously amid these shifts in monetary policy.