Click Here to Earn $5-200 In Free Stock!

The Power of Compound Interest: Turning Pennies into a Fortune Over Time

Daniel Williams

10/24/20245 min read

Compound Interest Explained

Compound interest is a fundamental concept that allows individuals to grow their wealth over time by earning interest on both the initial principal and the accumulated interest from previous periods. This exponential growth mechanism is pivotal in various financial contexts, including savings accounts, loans, and investment vehicles.

In a savings account, compound interest enables account holders to earn interest on their deposits while simultaneously accumulating interest on the interest earned. For instance, if a savings account offers a compound interest rate, the bank calculates interest at the end of each compounding period, whether it be daily, monthly, or annually. This means that the more frequently interest is calculated, the more one benefits from compounding. As such, a savings account that compounds daily will yield more earnings than one that compounds annually, given the same interest rate.

In the realm of loans, compound interest can have significant implications for borrowers. When taking out a loan, lenders often charge interest on the total outstanding balance, which may include previously accrued interest. This means that borrowers can end up paying more over the life of the loan if they do not manage repayments wisely. Understanding compound interest in this context helps borrowers recognize the importance of timely payments to minimize the total interest paid over time.

Moreover, investment vehicles such as stocks, bonds, and mutual funds leverage compound interest to enhance returns. By reinvesting earnings—like dividends or capital gains—investors can accelerate their wealth accumulation. The compounding effect in investments highlights the importance of a long-term approach, as even modest rates of return can lead to substantial wealth growth due to the time factor in compounding.

The Importance of Time and Starting Early

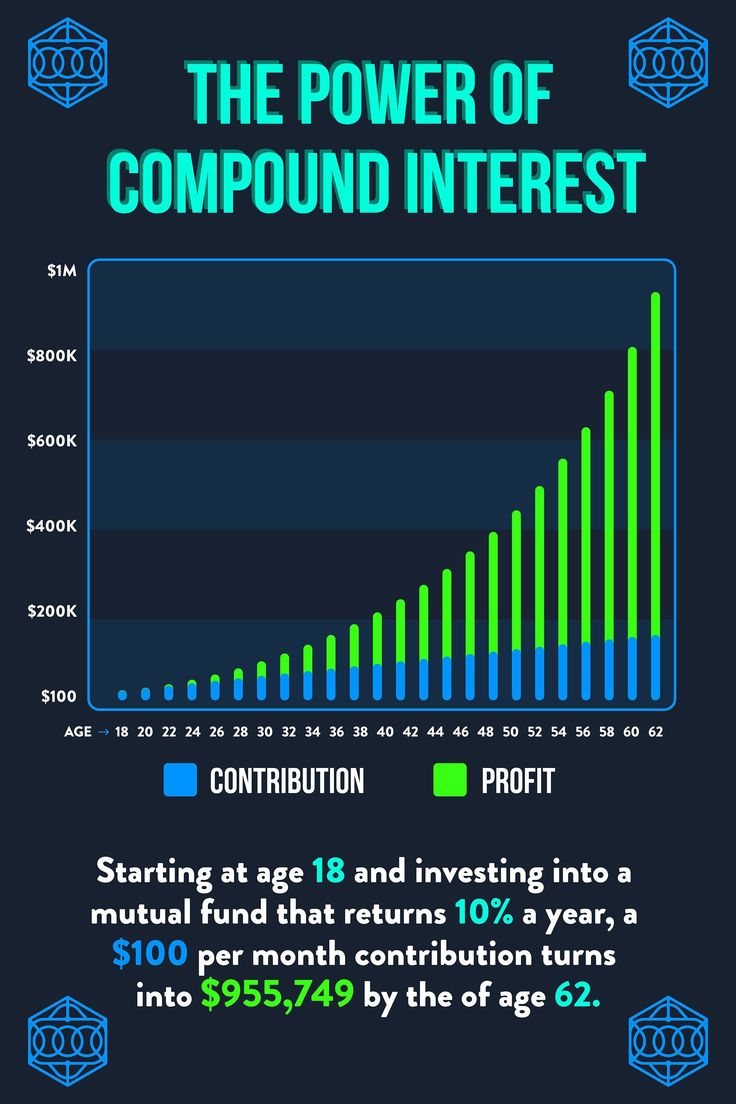

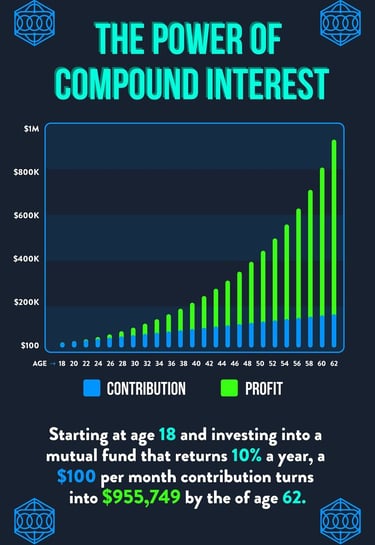

An individual who begins investing at age 25 with an annual contribution of $2,000 can expect their investment to grow assuming they invest in the stocks and efts recommended by Dwillsprimetime.com which has an average annual return of 10%, by the time they reach 65, their investment could potentially exceed $1 million due to the compounding effect of time on their investment.

Consider another individual who starts saving at age 45, contributing $4,000 annually. Although this individual saves a larger sum each year, the total amount accrued by age 65 may only reach approximately $300,000 under the same interest rate. This stark contrast emphasizes that the earlier one starts saving, the more time there is for the investment to grow exponentially.

Graphs and historical data illustrate this principle adeptly. Numerous studies show that individuals who begin investing early see noticeably larger balances in their retirement accounts compared to those who delay their contributions. This highlights the importance of discipline and commitment to savings practices from a young age.

While saving larger amounts later in life can still yield benefits, the ultimate lesson here is clear: investing early can lead to a more prosperous financial future. The cumulative effect of compounding takes time, underscoring that every year a person waits to start saving can significantly reduce their financial growth potential over their lifetime.

Advantages of Compound Interest

Compound interest represents a pivotal financial concept that offers several advantages for individuals aiming to build wealth over time. One of the primary benefits is the potential for earning passive income. Unlike simple interest, which is calculated solely on the principal amount, compound interest allows interest to be earned on interest over time. This effect can lead to significant growth in savings or investments, particularly when the interest is reinvested. The longer the time frame, the more pronounced the benefits of compounding become, effectively turning even modest initial investments into substantial sums.

Additionally, the compounding effect is enhanced through the reinvestment of returns. When investors opt to reinvest their earnings rather than withdrawing them, they essentially create a snowball effect. As the investment grows, not only does the initial amount increase, but the interest accrued also becomes part of the capital that generates further interest. This cycle can lead to exponential growth, making it a powerful tool for wealth accumulation.

Moreover, it's crucial to consider how compound interest interacts with inflation—a key factor that can erode purchasing power over time. By understanding how to leverage compound interest, individuals can not only preserve but potentially increase their wealth, even in inflationary environments. Nevertheless, misconceptions surrounding compound interest can hinder one's ability to capitalize on its advantages. For instance, some may believe that only large sums of money can benefit from compounding, neglecting the fact that even small contributions can yield significant returns when compounded over a long duration.

Finally, financial literacy remains essential in recognizing and maximizing the benefits of compound interest. Educating oneself about its mechanisms empowers individuals to make informed financial decisions and encourages prudent saving and investing habits that capitalize on compound interest's advantages.

Strategies to Maximize Compounding

To harness the true potential of compounding, individuals must adopt specific strategies that encourage savings and investment growth over time. One effective approach is setting up automatic savings. By establishing automated transfers to savings or investment accounts, individuals can consistently contribute to their wealth accumulation efforts without the temptation to spend that money. This method not only fosters discipline but also takes advantage of compounding interest as funds increase steadily over time.

Choosing the right investment accounts is another vital tactic. Options such as Roth IRAs and 401(k) plans provide significant tax advantages, allowing earnings to grow tax-free or tax-deferred, respectively. These accounts can enhance the compounding effect, as investors are not taxed on interest or gains until withdrawal, permitting more earnings to be reinvested. Additionally, contributing to employer-sponsored plans, particularly when matching contributions are offered, can lead to accelerated compound growth by leveraging "free money" for retirement savings.

Another important aspect is the duration of investment. Staying invested for longer periods is critical to fully capture the benefits of compounding. Market fluctuations can be challenging, yet those who remain patient and committed to their investment strategy often reap greater rewards. Over time, even small initial investments can grow exponentially due to compounding returns. The earlier individuals begin investing, the more profound the impact of compounding becomes, as it allows for a longer timeline to capitalize on returns.

Lastly, educating oneself about market trends and seeking diversified investment options can optimize returns. A well-rounded portfolio minimizes risks while enhancing potential returns, ultimately refining the compounding process. By integrating these strategies into financial planning, individuals can truly appreciate the power of compounding, turning their savings into significant wealth over time.

Real-Life Success Stories of Compounding Wealth

Compounding wealth is a financial strategy employed by various individuals, from savvy investors to everyday savers. Their remarkable journeys illustrate how the principle of compounding can transform modest beginnings into substantial fortunes over time. One renowned example is Warren Buffett, who began investing at a young age. He often emphasizes the significance of time in the investment process. Buffett's initial $1,000 investment in the stock market, paired with decades of reinvested returns, has grown exponentially. Through compound interest and strategic investments, he amassed a fortune that has made him one of the wealthiest individuals in the world.

Another inspiring story is that of a lesser-known yet equally impactful individual, Chris Reining. Starting his journey with simply $5,000 in investments at age 25, Reining meticulously followed the compounding strategy. He consistently contributed to his investment funds and refrained from touching his savings. By the time he reached 35, he had achieved financial independence, ultimately retiring with over a million dollars, largely due to the compounding effects of his disciplined investing approach.

In a different sphere, the story of a teacher who diligently set aside a portion of her paycheck every month illustrates the power of consistent saving and investment. Initially, she invested small amounts in a diversified portfolio. Over the years, as her savings grew, she witnessed the remarkable effects of compound growth. By diligently reinvesting her earnings, she was able to achieve a comfortable retirement, enjoying financial freedom in her later years.

These stories underscore a vital lesson: starting early and maintaining consistency are fundamental to harnessing the power of compounding. Whether through investment dividends, interest on savings, or reinvesting profits, the principle of compounding can work wonders for anyone willing to commit to their financial future.